The Data Infrastructure Thesis: Why Agricultural Finance is a Platform Problem, Not a Credit Problem

The agricultural finance gap is not an unsolvable development challenge. It's an infrastructure problem with a clear engineering solution. The technology exists. The business model is proven. The capital is available.

Kipyegon Bett

2/12/20265 min read

For decades, a ton of projects and research have gone into solving the issue of financing the African farmer. This article doesn’t ignore all that hard work; rather it builds upon decades of data from that entire endeavour. It seeks to provide a solution to the persistent misconception in development finance: the ‘unbankable’ African farmer. This narrative has dominated agricultural policy for years, shaping how billions of dollars in development capital are allocated. This article sees it as fundamentally wrong.

The problem is not that smallholder farmers are unbankable. The problem is that we are trying to apply industrial-era credit assessment frameworks to a 21st-century data problem. Traditional financial institutions look for collateral: title deeds, asset registries and formal employment records. Farmers have none of these. On the flip side, farmers do generate data. We just need to build the infrastructure to capture and monetize it.

This is not a minor technical distinction. It is the difference between a $170 billion financing gap that persists indefinitely and a massive platform opportunity waiting to be captured.

The Real Problem: Information Asymmetry at Scale

A functioning credit market requires three things: a way to assess risk, a mechanism to price it, and a system to monitor repayment. In developed markets, this infrastructure is built on credit bureaus, standardized financials, and legal frameworks for collateral seizure.

Only 6% of African smallholder farmers have access to credit and bank lending to agriculture accounts for less than 5% of total loan portfolios. Why? Because the infrastructure doesn't exist.

A smallholder farmer has no credit history, no formal employment record and no evidence of constant income. From a banker's perspective, they are a black box. The cost to manually underwrite a $500 loan exceeds the profit margin. The rational response is to decline.

This creates three cascading failures:

The Banker's Dilemma: Without data, there is no way to distinguish reliable borrowers from risky ones. The only rational response is blanket rejection or punitive interest rates that price in maximum uncertainty. Commercial banks perceive smallholder farmers as high-risk borrowers due to climate variability and lack of collateral, leading to systematic exclusion from formal credit markets.

The Aggregator's Death Spiral: This upstream credit constraint destroys the business model of agricultural aggregators; the critical intermediaries we discussed in the previous article. When farmers lack working capital, they must sell immediately at harvest to whoever offers cash on the spot. This ‘side-selling’ makes aggregator supply chains unpredictable, which makes aggregators themselves appear high-risk to lenders, perpetuating the capital black hole.

The Failure of Substitutes: Asset-based lending, government subsidies, and simple mobile money have all failed to scale because they treat the symptom (lack of cash) without solving the root cause: the information gap that makes farmers opaque to formal finance.

The result is a massive market failure. Farmers who could profitably deploy capital at 15-20% returns cannot access credit at any price.

The Reframe: Data as the New Collateral

Here is the critical insight: a farmer's true creditworthiness is not reflected in what they own; it is reflected in what they do.

A title deed is a static measure of an asset that may or may not generate cash flow. But a farmer's operational history; yield consistency, payment reliability, input adoption, supply commitments, is a dynamic, real-time measure of their ability to generate returns.

This leads to a new thesis: Data is the new collateral.

The most valuable asset in the agricultural value chain is a verifiable, continuous, digital record of operational performance. When you capture and structure this data properly, you transform it into what I call a Digital Trust Profile; a data-backed picture of risk that makes credit decisions faster, cheaper, and safer.

The specific data points that predict creditworthiness:

Historical yield data across multiple seasons

Consistency of supply to aggregators or buyers

Payment reliability for inputs and services

Operational excellence in farming practices

Transaction patterns and cash flow management

Each is measurable, verifiable, and predictive. Collectively, they provide far more signal about credit risk than a disputed land title.

Companies like Harvesting Inc. and Apollo Agriculture are already proving this works, using satellite data, yields, and transaction histories with machine learning to assess creditworthiness. Alternative credit scoring has achieved near 100% repayment rates in some value chains.

The technology exists. What's missing is the infrastructure layer that generates this data at scale.

The Infrastructure Stack: Physical, Financial, and Digital

Making this work requires three complementary layers working together:

Layer 1: Physical Infrastructure

IoT-based sensor networks now monitor soil moisture, pH, temperature, and nutrients in real-time, operating in remote areas through LoRaWAN protocols. Hyper-local weather stations provide data on rainfall and climate patterns. Weighbridge integrations and satellite remote sensing verify actual yields. Solar irrigation systems track water and energy usage.

The cost barrier has collapsed; sensor prices have dropped 70-80% in the past decade. IoT and AI integration in agriculture now enables real-time monitoring at price points accessible for small-scale operations.

Layer 2: Financial Infrastructure

Physical sensors only create value when connected to capital. This requires embedded lending platforms where credit decisions happen automatically based on Digital Trust Profiles. Dynamic pricing models using machine learning adjust rates based on verified performance; farmers with proven track records get dramatically better terms. Value chain financing structures products around entire supply chains rather than individual farmers, reducing risk while improving capital efficiency.

Layer 3: Digital Operations Platform

This is the connective tissue: farmer registries creating digital identities, transaction recording systems capturing every input purchase and harvest sale, analytics engines processing data to generate real-time credit scores, and API infrastructure allowing financial institutions to access farmer profiles and aggregators to verify commitments.

The critical insight: these three layers are complementary, not substitutable. You cannot fix agricultural finance with only IoT, only credit algorithms, or only digital payments. All three must work together because each unlocks the others. This is a coordination problem requiring a bundled approach.

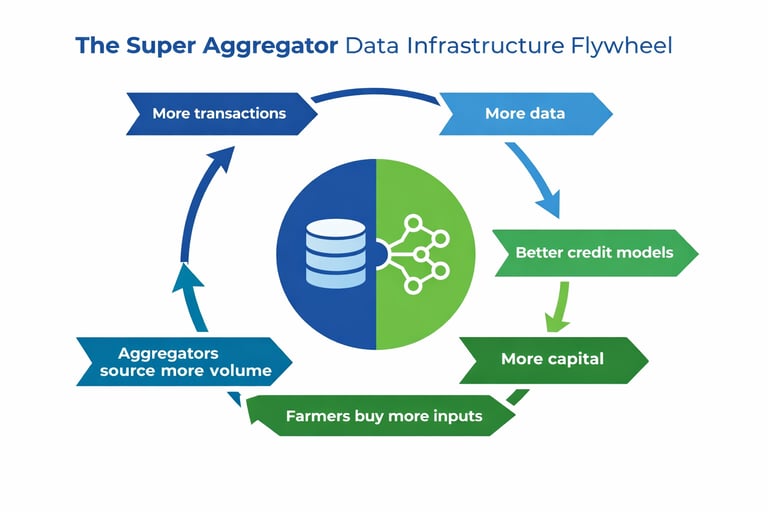

The Symbiotic Engine: Why Super Aggregators Generate the Data

A data infrastructure platform needs a continuous, high-volume source of quality transactional data. This is where Super Aggregators become essential. Their core business: sourcing commodities, providing inputs, paying farmers, is the data generation engine.

Every transaction creates data points: input purchases show adoption patterns, quality testing reveals yield performance, payment flows demonstrate reliability, delivery schedules prove consistency.

More transactions → more data → better credit models → more capital → farmers buy more inputs → aggregators source more volume. This is the flywheel.

Photo by Markus Winkler on Unsplash

The beauty: data generation becomes a byproduct of commercial transactions farmers want anyway. They want quality inputs, fair prices, reliable buyers. The Super Aggregator provides this, and the data infrastructure captures the resulting flows.

This is why Super Aggregator + Data Infrastructure is defensible in ways that simple aggregation is not. The aggregator that owns the data layer owns the customer relationship, the financial transaction, and the market intelligence. This is not margin enhancement—it's a different business model entirely.

The Path Forward

The agricultural finance gap is not an unsolvable development challenge. It's an infrastructure problem with a clear engineering solution. The technology exists. The business model is proven. The capital is available (I can’t authoritatively speak for funding though).

What's required is recognizing the problem correctly: not a failure of farmers or lenders, but a missing layer of data infrastructure that prevents an otherwise functional market from clearing.

Breaking this myth of the ‘unbankable farmer’ requires building infrastructure that makes farmers' operational performance visible, verifiable, and valuable. Companies like Apollo Agriculture and Harvesting are already doing this at scale, proving that when you solve the information asymmetry problem through data infrastructure, agricultural finance becomes not just viable but highly profitable.

The farmers were never the problem. The infrastructure was. And infrastructure, unlike changing human behavior or weather patterns, is something we can actually build.